The Psychology of Money by Morgan Housel — Notes

24 min readOct 21, 2020

Top Highlights

- “A genius is the man who can do the average thing when everyone else around him is losing his mind.” — Napoleon

- “The world is full of obvious things which nobody by any chance ever observes.” — Sherlock Holmes

- Financial outcomes are driven by luck, independent of intelligence and effort.

- Physics is guided by laws. Finance is guided by people’s behaviours.

- “History never repeats itself; man always does.” — Voltaire

- Your personal experiences with money make up maybe 0.00000001% of what’s happened in the world, but maybe 80% of how you think the world works

- “Some lessons have to be experienced before they can be understood.” — Michael Batnick

- “Nothing is as good or as bad as it seems.” — Scott Galloway

- Risk and luck are doppelgangers

- “The customer is always right” and “customers don’t know what they want” are both accepted business wisdom.

- The line between “inspiringly bold” and “foolishly reckless” can be a millimeter thick and only visible with hindsight

- Not all success is due to hard work, and not all poverty is due to laziness.

- Failure can be a lousy teacher, because it seduces smart people into thinking their decisions were terrible when sometimes they just reflect the unforgiving realities of risk.

- Modern capitalism is a pro at two things: Generating wealth and generating envy.

- Happiness is just results minus expectations.

- Warren Buffett’s net worth is $84.5 billion. Of that, $84.2 billion (99%) was accumulated after his 50th birthday. $81.5 billion (97%) came after he qualified for Social Security, in his mid-60s.

- Linear thinking is so much more intuitive than exponential thinking. If I ask you to calculate 8+8+8+8+8+8+8+8+8 in your head, you can do it in a few seconds (it’s 72). If I ask you to calculate 8×8×8×8×8×8×8×8×8, your head will explode (it’s 134,217,728).

- Preventing one desperate, ill-timed stock sale can do more for your lifetime returns than picking dozens of big-time winners.

- You need short-term paranoia to keep you alive long enough to exploit long-term optimism.

- You can be wrong half the time and still make a fortune.

- Perhaps 99% of the works of an art dealer acquired in his life turned out to be of little value. But that doesn’t particularly matter if the other 1% turn out to be the work of someone like Picasso.

- Anything that is huge, profitable, famous, or influential is the result of a tail event — an outlying one-in-thousands or millions event.

- Your success as an investor will be determined by how you respond to punctuated moments of terror, not the years spent on cruise control.

- Tails drive everything in business, investing, and finance. You realize that it’s normal for lots of things to go wrong, break, fail, and fall.

- Spending money to show people how much money you have is the fastest way to have less money.

- Wealth is the nice cars not purchased. The diamonds not bought. The watches not worn, the clothes forgone and the first-class upgrade declined.

- Having more control over your time and options is becoming one of the most valuable currencies in the world.

- Aiming to be mostly reasonable works better than trying to be coldly rational.

- “You can be risk loving and yet completely averse to ruin.” — Nassim Taleb

- Optimism sounds like a sales pitch. Pessimism sounds like someone trying to help you.

- “For reasons I have never understood, people like to hear that the world is going to hell.” — Historian Deirdre McCloskey

- Pessimism just sounds smarter and more plausible than optimism.

- Progress happens too slowly to notice, but setbacks happen too quickly to ignore.

- There are lots of overnight tragedies. There are rarely overnight miracles.

- Growth is driven by compounding, which always takes time. Destruction is driven by single points of failure, which can happen in seconds, and loss of confidence, which can happen in an instant.

- Pessimism is seductive because expecting things to be bad is the best way to be pleasantly surprised when they’re not.

- The illusion of control is more persuasive than the reality of uncertainty.

- “True success is exiting some rat race to modulate one’s activities for peace of mind.” — Nassim Taleb

- “I can afford to not be the greatest investor in the world, but I can’t afford to be a bad one.” — Morgan Housel

Introduction: The Greatest Show on Earth

- Financial outcomes are driven by luck, independent of intelligence and effort.

- Physics is guided by laws. Finance is guided by people’s behaviours.

- “History never repeats itself; man always does.” — Voltaire

1. No One’s Crazy

- Your personal experiences with money make up maybe 0.00000001% of what’s happened in the world, but maybe 80% of how you think the world works

- “some lessons have to be experienced before they can be understood.” — Michael Batnick

- Dogs were domesticated 10,000 years ago and still retain some behaviors of their wild ancestors. Yet here we are, with between 20 and 50 years of experience in the modern financial system, hoping to be perfectly acclimated.

2. Luck & Risk

- “Nothing is as good or as bad as it seems.” — Scott Galloway

- Someone else’s failure is usually attributed to bad decisions, while your own failures are usually chalked up to the dark side of risk.

- The cover of Forbes magazine does not celebrate poor investors who made good decisions but happened to experience the unfortunate side of risk. But it almost certainly celebrates rich investors who made OK or even reckless decisions and happened to get lucky. Both flipped the same coin that happened to land on a different side.

- Risk and luck are doppelgangers

- “The customer is always right” and “customers don’t know what they want” are both accepted business wisdom.

- The line between “inspiringly bold” and “foolishly reckless” can be a millimeter thick and only visible with hindsight

- Be careful who you praise and admire. Be careful who you look down upon and wish to avoid becoming.

- Not all success is due to hard work, and not all poverty is due to laziness.

- Focus less on specific individuals and case studies and more on broad patterns.

- Studying a specific person can be dangerous because we tend to study extreme examples — the billionaires, the CEOs, or the massive failures that dominate the news — and extreme examples are often the least applicable to other situations, given their complexity. The more extreme the outcome, the less likely you can apply its lessons to your own life, because the more likely the outcome was influenced by extreme ends of luck or risk.

- Trying to emulate Warren Buffett’s investment success is hard, because his results are so extreme that the role of luck in his lifetime performance is very likely high, and luck isn’t something you can reliably emulate. But realizing, that people who have control over their time tend to be happier in life is a broad and common enough observation that you can do something with it.

- Failure can be a lousy teacher, because it seduces smart people into thinking their decisions were terrible when sometimes they just reflect the unforgiving realities of risk.

3. Never Enough

- To make money they didn’t have and didn’t need, they risked what they did have and did need. And that’s foolish.

- If you risk something that is important to you for something that is unimportant to you.

- There is no reason to risk what you have and need for what you don’t have and don’t need.

- The hardest financial skill is getting the goalpost to stop moving.

- Modern capitalism is a pro at two things: Generating wealth and generating envy.

- Happiness is just results minus expectations.

- Social comparison is the problem here.

- “Enough” is not too little.

- There are many things never worth risking, no matter the potential gain.

4. Confounding Compounding

- Lessons from one field can often teach us something important about unrelated fields.

- Moderately cool summers, not cold winters, were the culprit for ice age. It begins when a summer never gets warm enough to melt the previous winter’s snow.

- “It is not necessarily the amount of snow that causes ice sheets but the fact that snow, however little, lasts.” —Gwen Schultz

- Warren Buffett’s net worth is $84.5 billion. Of that, $84.2 billion was accumulated after his 50th birthday. $81.5 billion came after he qualified for Social Security, in his mid-60s.

- Warren Buffett is a phenomenal investor. But you miss a key point if you attach all of his success to investing acumen. The real key to his success is that he’s been a phenomenal investor for three quarters of a century. Had he started investing in his 30s and retired in his 60s, few people would have ever heard of him.

- Buffett started investing at age 10. By age 30, he had a net worth of $1 million, or $9.3 million inflation-adjusted.

- If he was a normal person, and spent his teens and 20s exploring the world and finding his passion, he would have only $25000 by age 30. Even if generated 22% annual returns, and retired at 60 to play golf, his net worth would only be $11.9 million (99.9% less than current).

- Jim Simmons, head of hedge fund Renaissance Technologies generated 66% annual returns, thrice of Buffett’s 22%. His net worth is only $21 billion, 75% less than Buffett. This difference is due to the fact that Simmons found his investment stride at age 50. He’s had less than half as many years as Buffett to compound.

- If James Simons had earned his 66% annual returns for the 70-year span Buffett has built his wealth he would be worth — please hold your breath — sixty-three quintillion nine hundred quadrillion seven hundred eighty-one trillion seven hundred eighty billion seven hundred forty-eight million one hundred sixty thousand dollars.

- Linear thinking is so much more intuitive than exponential thinking. If I ask you to calculate 8+8+8+8+8+8+8+8+8 in your head, you can do it in a few seconds (it’s 72). If I ask you to calculate 8×8×8×8×8×8×8×8×8, your head will explode (it’s 134,217,728).

5. Getting Wealthy vs Staying Wealthy

- There are a million ways to get wealthy, and plenty of books on how to do so. But there’s only one way to stay wealthy: some combination of frugality and paranoia.

- Getting money is one thing. Keeping it is another.

- If I had to summarize money success in a single word it would be “survival.”

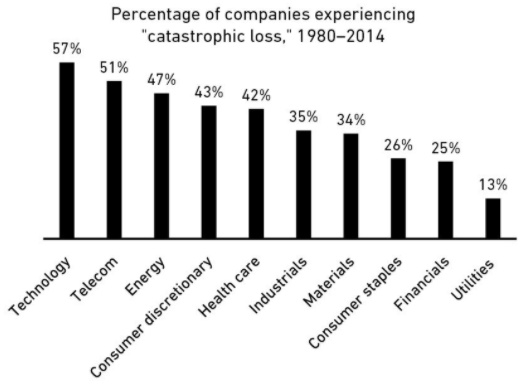

- 40% of companies successful enough to become publicly traded lost effectively all of their value over time. The Forbes 400 list of richest Americans has, on average, roughly 20% turnover per decade for causes that don’t have to do with death or transferring money to another family member.

- Capitalism is hard. But part of the reason this happens is because getting money and keeping money are two different skills.

- Getting money requires taking risks, being optimistic, and putting yourself out there. But keeping money requires the opposite of taking risk. It requires humility, and fear that what you’ve made can be taken away from you just as fast. It requires frugality and an acceptance that at least some of what you’ve made is attributable to luck, so past success can’t be relied upon to repeat indefinitely.

- Michael Moritz, the billionaire head of Sequoia Capital, was asked by Charlie Rose why Sequoia was so successful. Moritz mentioned longevity, noting that some VC firms succeed for five or ten years, but Sequoia has prospered for four decades.

- Moritz: I think we’ve always been afraid of going out of business.

- Few gains are so great that they’re worth wiping yourself out over.

- Compounding only works if you can give an asset years and years to grow. It’s like planting oak trees: A year of growth will never show much progress, 10 years can make a meaningful difference, and 50 years can create something absolutely extraordinary.

- We can spend years trying to figure out how Buffett achieved his investment returns: how he found the best companies, the cheapest stocks, the best managers. That’s hard. Less hard but equally important is pointing out what he didn’t do.

- He survived. Survival gave him longevity. And longevity — investing consistently from age 10 to at least age 89 — is what made compounding work wonders. That single point is what matters most when describing his success.

- Nassim Taleb put it this way: “Having an ‘edge’ and surviving are two different things: the first requires the second. You need to avoid ruin. At all costs.”

- More than I want big returns, I want to be financially unbreakable. And if I’m unbreakable I actually think I’ll get the biggest returns, because I’ll be able to stick around long enough for compounding to work wonders.

- Preventing one desperate, ill-timed stock sale can do more for your lifetime returns than picking dozens of big-time winners.

- Compounding doesn’t rely on earning big returns. Merely good returns sustained uninterrupted for the longest period of time — especially in times of chaos and havoc — will always win.

- Planning is important, but the most important part of every plan is to plan on the plan not going according to plan.

- Many bets fail not because they were wrong, but because they were mostly right in a situation that required things to be exactly right. Room for error — often called margin of safety — is one of the most underappreciated forces in finance. It comes in many forms: A frugal budget, flexible thinking, and a loose timeline — anything that lets you live happily with a range of outcomes.

- It’s different from being conservative. Conservative is avoiding a certain level of risk. Margin of safety is raising the odds of success at a given level of risk by increasing your chances of survival. Its magic is that the higher your margin of safety, the smaller your edge needs to be to have a favorable outcome.

- A barbelled personality — optimistic about the future, but paranoid about what will prevent you from getting to the future — is vital.

- You can be optimistic that the long-term growth trajectory is up and to the right, but equally sure that the road between now and then is filled with landmines, and always will be. Those two things are not mutually exclusive.

- By age 20 the average person can lose roughly half the synaptic connections they had in their brain at age two, as inefficient and redundant neural pathways are cleared out. But the average 20-year-old is much smarter than the average two-year-old. Destruction in the face of progress is not only possible, but an efficient way to get rid of excess.

- In last 170 years, standard of living improved 20 fold, but roughly 99.9% of companies went out of business, 33 recessions lasted a cumulative 48 years, stock market fell more than 10% 102 times, stocks lost third of their value 12 times.

- A mindset that can be paranoid and optimistic at the same time is hard to maintain, because seeing things as black or white takes less effort than accepting nuance.

- You need short-term paranoia to keep you alive long enough to exploit long-term optimism.

6. Tails, You Win

- You can be wrong half the time and still make a fortune.

- “I’ve been banging away at this thing for 30 years. I think the simple math is, some projects work and some don’t. There’s no reason to belabor either one. Just get on to the next.” — Brad Pitt

- Perhaps 99% of the works of an art dealer acquired in his life turned out to be of little value. But that doesn’t particularly matter if the other 1% turn out to be the work of someone like Picasso.

- Long tails — the farthest ends of a distribution of outcomes — have tremendous influence in finance, where a small number of events can account for the majority of outcomes.

- It is not intuitive that an investor can be wrong half the time and still make a fortune. It means we underestimate how normal it is for a lot of things to fail. Which causes us to overreact when they do.

- Anything that is huge, profitable, famous, or influential is the result of a tail event — an outlying one-in-thousands or millions event. And most of our attention goes to things that are huge, profitable, famous, or influential. When most of what we pay attention to is the result of a tail, it’s easy to underestimate how rare and powerful they are.

- If a VC makes 50 investments they likely expect half of them to fail, 10 to do pretty well, and one or two to be bonanzas that drive 100% of the fund’s returns.

- Out of more than 21,000 venture financings from 2004 to 2014: 65% lost money. Two and a half percent of investments made 10x–20x. One percent made more than a 20x return. Half a percent — about 100 companies out of 21,000 — earned 50x or more. That’s where the majority of the industry’s returns come from.

- The distribution of success among large public stocks over time is not much different than it is in venture capital.

- JP Morgan analyzed Russell 3000 index, since 1980. Forty percent of all Russell 3000 stock components lost at least 70% of their value and never recovered over this period. Effectively all of the index’s overall returns came from 7% of component companies that outperformed by at least two standard deviations.

- 4 in 10 public company stocks goes to zero over time.

- The Russell 3000 has increased more than 73-fold since 1980.

- Forty percent of the companies in the index were effectively failures. But the 7% of components that performed extremely well were more than enough to offset the duds.

- Not only do a few companies account for most of the market’s return, but within those companies are even more tail events.

- In 2018, Amazon drove 6% of the S&P 500’s returns. And Amazon’s growth is almost entirely due to Prime and Amazon Web Services, which itself are tail events in a company.

- Apple was responsible for almost 7% of the index’s returns in 2018. And it is driven overwhelmingly by the iPhone, which in the world of tech products is as tail-y as tails get.

- And who’s working at these companies? Google’s hiring acceptance rate is 0.2%. Facebook’s is 0.1%. Apple’s is about 2%. So the people working on these tail projects that drive tail returns have tail careers.

- Most financial advice is about today. What should you do right now, and what stocks look like good buys today? But most of the time today is not that important. Over the course of your lifetime as an investor the decisions that you make today or tomorrow or next week will not matter nearly as much as what you do during the small number of days — likely 1% of the time or less — when everyone else around you is going crazy.

- How you behaved as an investor during a few months in late 2008 and early 2009 will likely have more impact on your lifetime returns than everything you did from 2000 to 2008.

- “hours and hours of boredom punctuated by moments of sheer terror’. — pilot joke

- Your success as an investor will be determined by how you respond to punctuated moments of terror, not the years spent on cruise control.

- A good definition of an investing genius is the man or woman who can do the average thing when all those around them are going crazy. Tails drive everything.

- Tails drive everything in business, investing, and finance. You realize that it’s normal for lots of things to go wrong, break, fail, and fall.

- If you’re a good stock picker you’ll be right maybe half the time. If you’re a good business leader maybe half of your product and strategy ideas will work. If you’re a good investor most years will be just OK, and plenty will be bad. If you’re a good worker you’ll find the right company in the right field after several attempts and trials. And that’s if you’re good.

- “If you’re terrific in this business, you’re right six times out of 10” — Peter Lynch

- There are fields where you must be perfect every time. Flying a plane, for example. Then there are fields where you want to be at least pretty good nearly all the time. A restaurant chef.

- Investing, business, and finance are just not like these fields.

- At the Berkshire Hathaway shareholder meeting in 2013 Warren Buffett said he’s owned 400 to 500 stocks during his life and made most of his money on 10 of them. Charlie Munger followed up: “If you remove just a few of Berkshire’s top investments, its long-term track record is pretty average.”

- “It’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong. You can be wrong half the time and still make a fortune.” — George Soros

- There are 100 billion planets in our galaxy and only one, as far as we know, with intelligent life.

7. Freedom

- The ability to do what you want, when you want, with who you want, for as long as you want, is priceless. It is the highest dividend money pays.

- Using your money to buy time and options has a lifestyle benefit few luxury goods can compete with.

- If your job is to build cars, there is little you can do when you’re not on the assembly line. You detach from work and leave your tools in the factory. But if your job is to create a marketing campaign — a thought-based and decision job — your tool is your head, which never leaves you.

8. Man in the Car Paradox

- No one is impressed with your possessions as much as you are.

- people tend to want wealth to signal to others that they should be liked and admired. But in reality those other people often bypass admiring you, not because they don’t think wealth is admirable, but because they use your wealth as a benchmark for their own desire to be liked and admired.

- The letter I wrote after my son was born said, “You might think you want an expensive car, a fancy watch, and a huge house. But I’m telling you, you don’t. What you want is respect and admiration from other people, and you think having expensive stuff will bring it. It almost never does — especially from the people you want to respect and admire you.”

9. Wealth is what you don’t see

- Spending money to show people how much money you have is the fastest way to have less money.

- Modern capitalism makes helping people fake it until they make it a cherished industry.

- The truth is that wealth is what you don’t see.

- Wealth is the nice cars not purchased. The diamonds not bought. The watches not worn, the clothes forgone and the first-class upgrade declined.

10. Save Money

- The only factor you can control generates one of the only things that matters. How wonderful.

- The first idea — simple, but easy to overlook — is that building wealth has little to do with your income or investment returns, and lots to do with your savings rate.

- Past a certain level of income, what you need is just what sits below your ego.

- The world used to be hyper-local. Just over 100 years ago 75% of Americans had neither telephones nor regular mail service, according to historian Robert Gordon. That made competition hyper-local. A worker with just average intelligence might be the best in their town, and they got treated like the best because they didn’t have to compete with the smarter worker in another town.

- That’s now changed. A hyper-connected world means the talent pool you compete in has gone from hundreds or thousands spanning your town to millions or billions spanning the globe. This is especially true for jobs that rely on working with your head versus your muscles: teaching, marketing, analysis, consulting, accounting, programming, journalism, and even medicine increasingly compete in global talent pools. More fields will fall into this category as digitization erases global boundaries.

- “I’m smart” is increasingly a bad answer to that question, because there are a lot of smart people in the world. Almost 600 people ace the SATs each year. Another 7,000 come within a handful of points. In a winner-take-all and globalized world these kinds of people are increasingly your direct competitors.

- Intelligence is not a reliable advantage in a world that’s become as connected as ours has. But flexibility is. In a world where intelligence is hyper-competitive and many previous technical skills have become automated, competitive advantages tilt toward nuanced and soft skills — like communication, empathy, and, perhaps most of all, flexibility.

- Having more control over your time and options is becoming one of the most valuable currencies in the world.

11. Reasonable > Rational

- Aiming to be mostly reasonable works better than trying to be coldly rational.

- You’re not a spreadsheet. You’re a person. A screwed up, emotional person.

- A one-degree increase in body temperature has been shown to slow the replication rate of some viruses by a factor of 200.

- In the real world, people do not want the mathematically optimal strategy. They want the strategy that maximizes for how well they sleep at night.

- “minimizing future regret” is hard to rationalize on paper but easy to justify in real life. A rational investor makes decisions based on numeric facts. A reasonable investor makes them in a conference room surrounded by co-workers you want to think highly of you, with a spouse you don’t want to let down, or judged against the silly but realistic competitors that are your brother-in-law, your neighbour, and your own personal doubts. Investing has a social component that’s often ignored when viewed through a strictly financial lens.

- What’s often overlooked in finance is that something can be technically true but contextually nonsense.

- The historical odds of making money in U.S. markets are 50/50 over one-day periods, 68% in one-year periods, 88% in 10-year periods, and (so far) 100% in 20-year periods.

12. Surprise

- History is the study of change, ironically, used as a map of the future.

- “Things that have never happened before happen all the time.” — Scott Sagan

- If you view investing as a hard science, history should be a perfect guide to the future. Geologists can look at a billion years of historical data and form models of how the earth behaves. So can meteorologists. And doctors — kidneys operate the same way in 2020 as they did in 1020. Investing is not a hard science. It’s a massive group of people making imperfect decisions with limited information about things that will have a massive impact on their wellbeing, which can make even smart people nervous, greedy and paranoid.

- Fifteen billion people were born in the 19th and 20th centuries. But try to imagine how different the global economy — and the whole world — would be today if just seven of them never existed: Adolf Hitler, Joseph Stalin, Mao Zedong, Gavrilo Princip, Thomas Edison, Bill Gates, Martin Luther King. 0.00000000004% of people were responsible for perhaps the majority of the world’s direction over the last century.

- Imagine the last century without: The Great Depression, World War II, The Manhattan Project, Vaccines, Antibiotics, ARPANET, September 11th, The fall of the Soviet Union.

- The thing that makes tail events easy to underappreciate is how easy it is to underestimate how things compound.

- How, for example, 9/11 prompted the Federal Reserve to cut interest rates, which helped drive the housing bubble, which led to the financial crisis, which led to a poor jobs market, which led tens of millions to seek a college education, which led to $1.6 trillion in student loans with a 10.8% default rate.

- The average time between recessions has grown from about two years in the late 1800s to five years in the early 20th century to eight years over the last half-century.

- There are plenty of theories on why recessions have become less frequent. One is that the Fed is better at managing the business cycle, or at least extending it. Another is that heavy industry is more prone to boom-and-bust overproduction than the service industries that dominated the last 50 years.

- The pessimistic view is that we now have fewer recessions, but when they occur they are more powerful than before.

- Benjamin Graham advocated purchasing stocks trading for less than their net working assets — basically cash in the bank minus all debts. This sounds great, but few stocks actually trade that cheaply anymore — other than, say, a penny stock accused of accounting fraud.

13. Room for error

- The most important part of every plan is planning on your plan not going according to plan.

- “the purpose of the margin of safety is to render the forecast unnecessary.”

- Room for error lets you endure a range of potential outcomes, and endurance lets you stick around long enough to let the odds of benefiting from a low-probability outcome fall in your favor.

- The biggest gains occur infrequently, either because they don’t happen often or because they take time to compound.

- “You can be risk loving and yet completely averse to ruin.” — Nassim Taleb

- The ability to do what you want, when you want, for as long as you want, has an infinite ROI.

14. You’ll Change

- Long term planning is harder than it seems because people’s goals and desires change over time

- Imagining a goal is easy and fun. Imagining a goal in the context of the realistic life stresses that grow with competitive pursuits is something entirely different.

- It’s hard to make enduring long-term decisions when your view of what you’ll want in the future is likely to shift.

- young people pay good money to get tattoos removed that teenagers paid good money to get. Middle-aged people rushed to divorce people who young adults rushed to marry. Older adults work hard to lose what middle-aged adults worked hard to gain.

- rather than one 80-something-year lifespan, our money has perhaps four distinct 20-year blocks.

- Sunk costs — anchoring decisions to past efforts that can’t be refunded — are a devil in a world where people change over time. They make our future selves prisoners to our past, different, selves. It’s the equivalent of a stranger making major life decisions for you.

15. Nothing’s free

- Everything has a price, but not all prices appear on labels.

- The S&P 500 increased 119-fold in the 50 years ending 2018. All you had to do was sit back and let your money compound.

- successful investing demands a price. But its currency is not dollars and cents. It’s volatility, fear, doubt, uncertainty, and regret — all of which are easy to overlook until you’re dealing with them in real time.

- Netflix stock returned more than 35,000% from 2002 to 2018, but traded below its previous all-time high on 94% of days.

- Monster Beverage returned 319,000% from 1995 to 2018 — among the highest returns in history — but traded below its previous high 95% of the time during that period.

- thinking of market volatility as a fee rather than a fine is an important part of developing the kind of mindset that lets you stick around long enough for investing gains to work in your favor.

16. You & Me

- Beware taking financial cues from people that are playing a different game than you are.

- Bubbles form when the momentum of short-term returns attracts enough money that the makeup of investors shifts from mostly long term to mostly short term.

- That process feeds on itself. As traders push up short-term returns, they attract even more traders. Before long — and it often doesn’t take long — the dominant market price-setters with the most authority are those with shorter time horizons.

17. The seduction of pessimism

- Optimism sounds like a sales pitch. Pessimism sounds like someone trying to help you.

- “For reasons I have never understood, people like to hear that the world is going to hell.” — Historian Deirdre McCloskey

- Optimism is the best bet for most people because the world tends to get better for most people most of the time.

- Pessimism isn’t just more common than optimism. It also sounds smarter. It’s intellectually captivating, and it’s paid more attention than optimism, which is often viewed as being oblivious to risk.

- Real optimists don’t believe that everything will be great. That’s complacency. Optimism is a belief that the odds of a good outcome are in your favor over time, even when there will be setbacks along the way.

- “I am not an optimist. I am a very serious possibilist.” — Hans Rosling

- Pessimism just sounds smarter and more plausible than optimism.

- “I have observed that not the man who hopes when others despair, but the man who despairs when others hope, is admired by a large class of persons as a sage.” — John Stuart Mill

- Organisms that treat threats as more urgent than opportunities have a better chance to survive and reproduce.

- extremely good and extremely bad circumstances rarely stay that way for long because supply and demand adapt in hard-to-predict ways.

- Progress happens too slowly to notice, but setbacks happen too quickly to ignore.

- There are lots of overnight tragedies. There are rarely overnight miracles.

- Growth is driven by compounding, which always takes time. Destruction is driven by single points of failure, which can happen in seconds, and loss of confidence, which can happen in an instant.

- It’s easier to create a narrative around pessimism because the story pieces tend to be fresher and more recent.

- Optimistic narratives require looking at a long stretch of history and developments, which people tend to forget and take more effort to piece together.

- Consider the progress of medicine. Looking at the last year will do you little good. Any single decade won’t do much better. But looking at the last 50 years will show something extraordinary.

- In stock markets, a 40% decline that takes place in six months will draw congressional investigations, but a 140% gain that takes place over six years can go virtually unnoticed.

- In careers, where reputations take a lifetime to build and a single email to destroy.

- The short sting of pessimism prevails while the powerful pull of optimism goes unnoticed.

- In investing you must identify the price of success — volatility and loss amid the long backdrop of growth — and be willing to pay it.

- Expecting things to be great means a best-case scenario that feels flat. Pessimism reduces expectations, narrowing the gap between possible outcomes and outcomes you feel great about.

- Pessimism is seductive because expecting things to be bad is the best way to be pleasantly surprised when they’re not.

18. When you’ll believe anything

- The more you want something to be true, the more likely you are to believe a story that overestimates the odds of it being true.

- Hindsight, the ability to explain the past, gives us the illusion that the world is understandable. It gives us the illusion that the world makes sense, even when it doesn’t make sense. That’s a big deal in producing mistakes in many fields. — Daniel Kahneman

- We all want the complicated world we live in to make sense. So we tell ourselves stories to fill in the gaps of what are effectively blind spots.

- “Risk is what’s left over when you think you’ve thought of everything.” — Carl Richards

- “We need to believe we live in a predictable, controllable world, so we turn to authoritative-sounding people who promise to satisfy that need.” — Philip Tetlock

- The illusion of control is more persuasive than the reality of uncertainty.

- When planning we focus on what we want to do and can do, neglecting the plans and skills of others whose decisions might affect our outcomes.

19. All Together Now

- Become OK with a lot of things going wrong. You can be wrong half the time and still make a fortune, because a small minority of things account for the majority of outcomes.

20. Confessions

- Half of all U.S. mutual fund portfolio managers do not invest a cent of their own money in their funds, according to Morningstar.

- Important financial decisions are not made in spreadsheets or in textbooks. They are made at the dinner table. They often aren’t made with the intention of maximizing returns, but minimizing the chance of disappointing a spouse or child.

- “True success is exiting some rat race to modulate one’s activities for peace of mind.” — Nassim Taleb

- “I can afford to not be the greatest investor in the world, but I can’t afford to be a bad one.” — Morgan Housel